SOX Testing plays a critical role in maintaining strong financial governance, operational discipline, and organizational credibility. It refers to the processes used to validate a company’s compliance with the Sarbanes‑Oxley Act (SOX) of 2002—legislation established to protect investors from fraudulent financial reporting. SOX Testing evaluates both the design and operating effectiveness of Internal Controls Over Financial Reporting (ICFR).

Integrating SOX testing with IT General Controls (ITGC) and IT Application Controls (ITAC) is essential because financial reporting depends on secure, well‑controlled, and reliable systems. ITGC ensures the overall integrity of the system environment, while ITAC provides assurance that automated financial processes operate accurately and consistently. When combined, they strengthen the control environment, reduce risk, improve compliance efficiency, and provide reliable end‑to‑end assurance over financial data.

A key benefit of integration is clearer deficiency evaluation. Weak ITGCs often invalidate reliance on automated application controls, forcing expanded manual testing and increasing the risk of significant deficiencies or material weaknesses.

Cross‑functional Ownership Is Essential

An integrated SOX approach depends on collaboration across multiple functions:

- Finance teams

- IT operations

- Security teams

- Business application owners

These teams must align on a unified testing calendar, shared evidence repositories, and standardized documentation practices. This coordination enhances audit efficiency, reduces control failures, and improves overall assurance.

SOX Scoping: The Foundation of an Integrated Approach

Integration begins with mapping financial processes to the systems that support them. This includes identifying applications that materially impact financial reporting and aligning them with the relevant ITGC domains. Proper scoping ensures both ITGCs and ITACs are tested appropriately and prevents gaps or duplications during the audit cycle.

Integrated testing improves evidence quality. When ITGC and ITAC testing are aligned, organizations can produce audit‑ready evidence that meets standards for precision, completeness, and timing—reducing audit follow‑ups and re‑performance.

Automating SOX testing with ITGC and ITACs delivers significant improvements in accuracy, efficiency, control reliability, and audit readiness. Automated integration refers to using technology to connect SOX testing processes with the underlying IT General Controls (ITGC) and IT Application Controls (ITAC). Instead of manually gathering evidence, testing controls, or tracking exceptions, organizations use tools like GRC platforms, automated monitoring tools, workflow engines, and RPA to streamline or fully automate the process.

This type of integration enables continuous control monitoring, near real-time evidence collection, and exception flagging without manual intervention.

An integrated SOX testing model is especially critical under SOX 404, where management must assert ICFR effectiveness and auditors rely on ITGCs to place reliance on automated controls.

Structured SOX Testing Flow

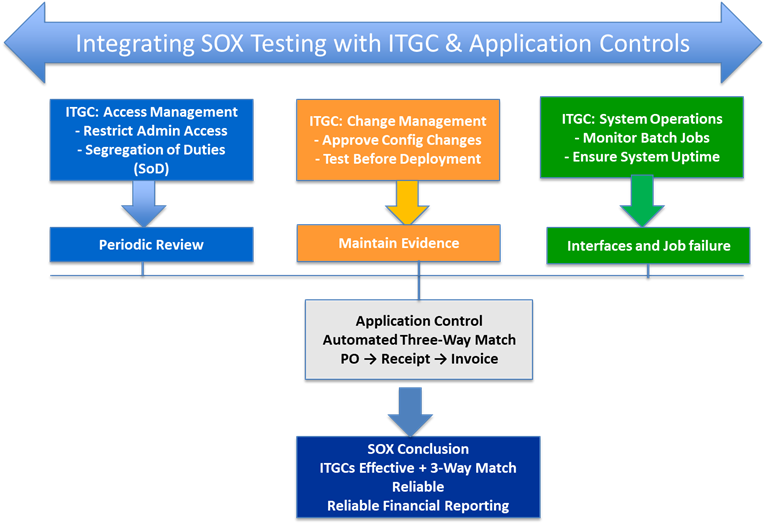

1.Assess ITGCs first

The effectiveness of automated application controls depends on strong ITGCs. If access, change, and operations controls are reliable, auditors can rely on system workflows—reducing manual testing and lowering audit costs.

2. Link application controls to supporting ITGCs

- Access Management → supports role‑based workflows

- Change Management → ensures configuration integrity

- IT Operations → ensures accurate batch processing

- Backup & Recovery → supports data completeness and availability

Scenario Example

Scenario: An organization uses an ERP system to process vendor invoices and supplier payments.

SOX Risk: Unauthorized or incorrect payments.

Risk mitigation requires:

ITGC Controls: Access Management, Change Management, IT Operations

ITAC Controls: Automated three‑way match (PO, GRN, invoice) to ensure only valid and accurate payments are processed

Conclusion

Integrating SOX testing with ITGC and ITAC builds a strong and reliable control environment. It ensures both the technology foundation and the automated processes supporting financial reporting are secure, effective, and resilient. While integration can introduce challenges—such as system complexity, technical evidence requirements, and cross‑functional coordination—the benefits far outweigh the effort. Ultimately, this integrated approach enhances audit efficiency, strengthens data integrity, supports accurate financial reporting, and reinforces confidence among stakeholders and regulators.